Jaga,

To focus on your excellent article of

Rana Foroohar in

Time magazine:

The majority of American citizens have plenty of concrete reasons for being uncomfortable with the country’s economic foundation. They worry about

their income (

job security),

pension,

health care,

social security,

savings, and

the future of their children and grand children. If the assistant managing editor in charge of economics and business of the respectable New York based news magazine

Time,

Rana Foroohar, states that "

The U.S. system of market capitalism itself is broken." then there must be some truth in that.

The nefarious condition of America's economy and thus system is very, very worrysome! In her book "

Makers and Takers: The Rise of Finance and the Fall of American Business", a three-year research and reporting effort

Rana Foroohar writes: '

Our economic illness has a name: financialization,' Her argument is that

finance for the sake of finance is bad for business -- and

capitalism as a whole.

Traditionally, finance served the needs of business (Foroohar's '

makers')

by providing capital and investing in long-term growth. But starting in the postwar decades and ramping up from

the Reagan era onward, finance (the '

takers') began to take care of No. 1 first.

America’s economic illness has a name:

financialization. It’s an academic term for the trend by which

Wall Street and its methods have come to reign supreme in America, permeating not just

the financial industry but also much of

American business. It includes everything from

the growth in size and

scope of finance and

financial activity in the economy; to

the rise of debt-fueled speculation over

productive lending; to the ascendancy of

shareholder value as

the sole model for corporate governance; to the proliferation of

risky,

selfish thinking in both the private and public sectors; to

the increasing political power of

financiers and

the CEOs they enrich; to the way in which a “

markets know best” ideology remains the status quo.

Financialization is a big, unfriendly word with broad, disconcerting implications.

Business has reoriented its orbit around

the financial sector when

financialization began its fastest growth, in the decades from the late 1970s onward.

The growing influence and financial power of Wall Street and

the rise of the ownership society has promoted

owning property and

further tied individual health care and retirement to the stock market.

The single biggest unexplored reason for long-term slower growth is that

the financial system has stopped serving the real economy and now serves mainly itself. A lack of real fiscal action on the part of politicians forced

the Fed to pump $4.5 trillion in monetary stimulus into the economy after 2008. This shows just

how broken the model is, since

the central bank’s best efforts have resulted in record stock prices (

which enrich mainly the wealthiest 10% of the population that owns more than 80% of all stocks) but also

a lackluster 2% economy with almost

no income growth.

Now, as many

top economists and

investors predict

an era of much lower asset-price returns over the next 30 years, America’s ability

to offer up even the appearance of growth—via financially oriented strategies like low interest rates, more and more consumer credit, tax-deferred debt financing for businesses, and asset bubbles that make people feel richer than we really are, until they burst—

is at an end.

Financialization Financialization

Financialization is

the financial capitalism that has developed over

the decades between

1980 and

2010, in which

financial leverage tended to override capital (

equity), and

financial markets tended to

dominate over the traditional industrial economy and

agricultural economics.

Financialization

Financialization describes

an economic system or process that attempts

to reduce all value that is exchanged (whether

tangible or

intangible,

future or

present promises, etc.) into

a financial instrument.

The intent of financialization is to be able

to reduce any work product or

service to

an exchangeable financial instrument, like

currency, and thus

make it easier for people to trade these financial instruments.

Workers, through

a financial instrument such as a

mortgage, may

trade their

promise of future work or

wages for

a home.

The financialization of risk sharing is what makes possible

all insurance.

The financialization of a government's promises (e.g.,

US government bonds) is what

makes possible all government deficit spending.

Financialization also

makes economic rents possible.

Over the past few decades,

finance has

turned away from this traditional role.

Academic research shows that

only a fraction of all the money washing around the financial markets these days actually makes it to Main Street businesses. “

The intermediation of household savings for productive investment in the business sector constitutes only a minor share of the business of banking today". Around

15% of capital coming from

financial institutions today is used to

fund business investments, whereas it would have been

the majority of what banks did earlier in

the 20th century.

The relationship between capital markets and businesses

The relationship between capital markets and businessesUntil the early seventies

Finance took individual and

corporate savings via

the unified national bond and banking system and funneled them into

productive enterprises,

creating new jobs,

new wealth and, ultimately,

economic growth. For the most part,

finance—which today includes everything from

banks and

hedge funds to

mutual funds,

insurance firms,

trading houses and such—

essentially served business. It was a vital organ but not, for the most part, the central one.

Adair Turner: “

Across all advanced economies, the role of the capital markets and the banking sector in funding new investment is decreasing.”

Most of the money in the system is being

used for

lending against existing assets such as

housing,

stocks and

bonds.

The financial sector now represents around 7% of the U.S. economy, up from about

4% in 1980. Despite currently

taking around 25% of all corporate profits,

it creates a mere 4% of all jobs. When

finance gets that big, it starts to suck the economic air out of the room.

Globally,

free-market capitalism is coming under fire, as

countries across Europe question its merits and emerging markets like

Brazil,

China and

Singapore run their own forms of state-directed capitalism. There is a need for a new and more inclusive type of capitalism, one that also helps businesses make better long-term decisions rather than focusing only on the next quarter.

Rana Foroohar, wondered why our market system doesn’t serve companies, workers and consumers better than it does. For some time now, finance has been thought by most to be at the very top of the economic hierarchy, the most aspirational part of an advanced service economy that graduated from agriculture and manufacturing. But research shows just how the unintended consequences of this misguided belief have endangered the very system America has prided itself on exporting around the world.

Rana Foroohar (born 1970) is an assistant managing editor for Time magazine. In the past, she was an economics and foreign editor at Newsweek, where she had previously worked as a London-based correspondent covering Europe and the Middle East. For this reporting, she received the German Marshall Fund's Peter R. Weitz Prize for transatlantic reporting. Foroohar was raised in Frankfort, Indiana. Foroohar is also a global economic analyst for CNN, a frequent commentator on NPR and a life member of the Council on Foreign Relations. Her book Makers and Takers went on sale May 17 from Crown Business. She graduated from Barnard College, Columbia University in 1992 with a B. A. in English literature. Foroohar resides in Brooklyn with her husband John Sedgwick and her two children, daughter Darya and son Alex.

Rana Foroohar (born 1970) is an assistant managing editor for Time magazine. In the past, she was an economics and foreign editor at Newsweek, where she had previously worked as a London-based correspondent covering Europe and the Middle East. For this reporting, she received the German Marshall Fund's Peter R. Weitz Prize for transatlantic reporting. Foroohar was raised in Frankfort, Indiana. Foroohar is also a global economic analyst for CNN, a frequent commentator on NPR and a life member of the Council on Foreign Relations. Her book Makers and Takers went on sale May 17 from Crown Business. She graduated from Barnard College, Columbia University in 1992 with a B. A. in English literature. Foroohar resides in Brooklyn with her husband John Sedgwick and her two children, daughter Darya and son Alex. (

iranian.com/main/blog/m-saadat-noury/first-iranian-female-who-has-become-famous-world-journalist-rana-foroohar.html )

The growth that America had enjoyed following World War II began to slow in the 1970s. Rather than make tough decisions like choosing among various interest groups, politicians decided to pass that responsibility to the financial markets. Little by little,

the Depression-era regulation that

had served America so well was rolled back, and

finance grew to become the dominant force that it is today.

The shifts were bipartisan, and to be fair they often seemed like good ideas at the time; but they also came with unintended consequences. Deregulation of interest rates opened the door to

a spate of financial “

innovations” and

a shift in bank function from lending to trading.

Reaganomics famously led to a number of other economic policies that favored

Wall Street.

Clinton-era deregulation, which seemed

a path out of the economic doldrums of

the late 1980s,

continued the trend. Loose monetary policy from

the Alan Greenspan era onward

created an environment in which easy money papered over underlying problems in the economy, so much so that it is now chronically dependent on near-zero interest rates to keep from falling back into recession.

Reaganomics Reaganomics

Reaganomics denotes the economic policies of

President Ronald Reagan in

the 1980s. He sought to remedy

the high inflation and

recessions of

the 1970s, which conservatives attributed to the heavy burden government imposed on private enterprise.

Reagan called for

sharp reductions in

federal taxes,

spending, and

regulation as well as

a monetary policy that

strictly limited the growth of the money supply.

Debt is the lifeblood of financeThe housing market

Debt is the lifeblood of financeThe housing market is divided into

two branches and

dependent on government life support,

the retirement system has left

millions insecure in their old age,

a tax code that favors debt over equity.

Debt is

the lifeblood of finance; with

the rise of the securities-and-trading portion of

the industry came

a rise in debt of all kinds,

public and

private.

Rising debt and

credit levels stoke

financial instability. And yet, as

finance has

captured a greater and greater piece of the national pie, it has, perversely, all but ensured that

debt is indispensable to maintaining any growth at all in

an advanced economy like the U.S., where

70% of output is consumer spending.

Debt-fueled finance has become a

sickishly sweet substitute for

the real thing, an

addiction that

just gets worse. (

The amount of credit offered to American consumers has doubled in real dollars since the 1980s, as have the fees they pay to their banks.)

Economist

Raghuram Rajan: "

Credit has become a palliative to address the deeper anxieties of downward mobility in the middle class." In his words, “

let them eat credit” could well summarize the mantra of the go-go years before the economic meltdown. And things have only deteriorated since, with global debt levels $57 trillion higher than they were in 2007.

The rise of finance has also distorted local economies. It’s the reason rents are rising in some communities where unemployment is still high. America’s housing market now favors cash buyers, since banks are still more interested in making profits by trading than by the traditional role of lending out our savings to people and businesses looking to make longterm investments (like buying a house), ensuring that younger people can’t get on the housing ladder.

Lending to small businessThis pinch is particularly evident in the tumult many American businesses face. Lending to small business has fallen particularly sharply, as has the number of startup firms. In the early 1980s, new companies made up half of all U.S. businesses. For all the talk of Silicon Valley startups, the number of new firms as a share of all businesses has actually shrunk. From 1978 to 2012 it declined by 44%, a trend that numerous researchers and even many investors and businesspeople link to the financial industry’s change in focus from lending to speculation. The wane in entrepreneurship means less economic vibrancy, given that new businesses are the nation’s foremost source of job creation and GDP growth. Buffett summed it up in his folksy way: “You’ve now got a body of people who’ve decided they’d rather go to the casino than the restaurant” of capitalism.

Startup company A startup company

A startup company (

startup or start-up) is an entrepreneurial venture typically describing newly emerged, fast-growing business. Definition of the startup usually refers to a company, a partnership or an organization designed to rapidly develop scalable business model. Often, startup companies deploy advanced technologies, such as Internet, communication, robotics, etc. These companies are generally involved in the design and implementation of the innovative processes of the development, validation and research for target markets. The term became internationally widespread during the dot-com bubble when a great number of dot-com companies were founded.

A startup is a company designed to grow fast. Being newly founded does not in itself make a company a startup. Nor is it necessary for a startup to work on technology, or take venture funding, or have some sort of "exit". The only essential thing is growth. Everything else we associate with startups follows from growth." Graham added that an entrepreneur starting a startup is committing to solve a harder type of problem than ordinary businesses do. "You're committing to search for one of the rare ideas that generates rapid growth."

tartup companies, particularly those associated with new technology, sometimes produce huge returns to their creators and investors—a recent example of such is Google, whose creators became billionaires through their stock ownership and options. However, the failure rate of startup companies is very high.

One common reason for failure is that startup companies can run out of funding, without securing their next round of investment or before becoming profitable enough to pay their staff. When this happens, it can leave employees without paychecks. Sometimes these companies are purchased by other companies, if they are deemed to be viable, but oftentimes they leave employees with very little recourse to recoup lost income for worked time.

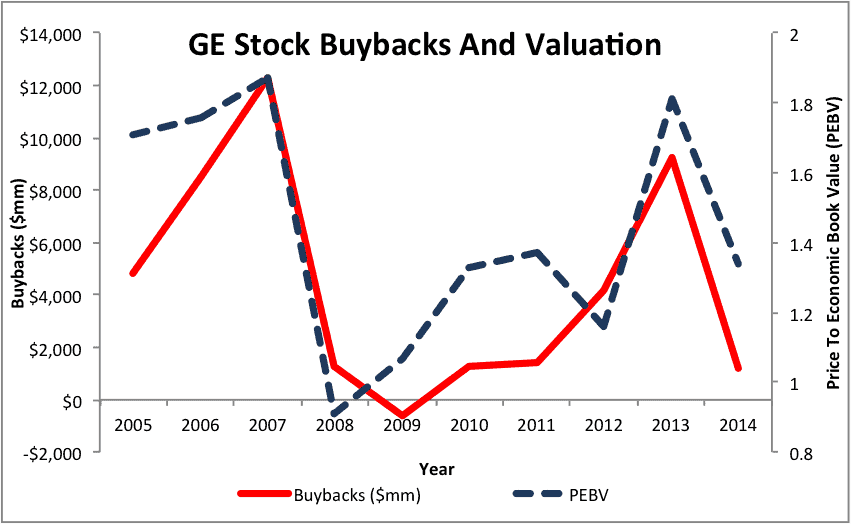

In

lobbying for

short-term share-boosting management,

finance is also largely responsible for

the drastic cutback in

research-and-development outlays in

corporate America, investments that are seed corn for future prosperity. Take share buybacks, in which a company—usually with some fanfare—goes to the stock market to purchase its own shares, usually at the top of

the market, and often as a way of artificially bolstering share prices in order to enrich investors and executives paid largely in stock options. Indeed, if you were to chart the rise in money spent on share buybacks and the fall in corporate spending on productive investments like

R&D, the two lines make a perfect

X. No sector has been immune, not even the ones we think of as the most innovative. Many tech firms, for example, spend far more on share-price boosting than on

R&D as a whole. The markets penalize them when they don’t.

As a result,

business dynamism, which is at

the root of economic growth, has suffered. The number of new initial public offerings (

IPOs) (

en.wikipedia.org/wiki/Initial_public_offering ) is about a third of what it was 20 years ago. True, the dollar value of

IPOs in

2014 was

$74.4 billion, up from

$47.1 billion in 1996. (The median

IPO rose to

$96 million from

$30 million during the same period.) This may show investors want to make only the surest of bets, which is not necessarily the sign of a vibrant market. But there’s another, more disturbing reason: firms simply don’t want to go public, lest their work become dominated by playing by

Wall Street’s rules rather than creating

real value.

Research and development

Research and development Research and development

Research and development (

R&D), also known in Europe as

research and technical (or technological)

development (

RTD), is a general term for activities in connection with corporate or governmental innovation.

Research and development is a component of

Innovation and is situated at the front end of

the Innovation life cycle.

Innovation builds on

R&D and includes

commercialization phases.

The activities that are classified as

R&D differ from company to company, but there are two primary models, with an

R&D department being either staffed by

engineers and tasked with directly developing

new products, or staffed with

industrial scientists and tasked with

applied research in

scientific or

technological fields which may facilitate

future product development. In either case,

R&D differs from the vast majority of corporate activities in that it is not often intended to yield immediate profit, and generally carries greater risk and an uncertain return on investment.

So innovation, Research and development are important for a vibrant Capitalist economy, competition, a stakeholders economy, but also for shareholders, who can win commercialy by new products that sell. An economy which is stuck in financial market thinking will stay behind, because risks will be avoided and investments in human capital, product development and innovation won't be made. Finance which serve the needs of business by providing capital and investing in long-term growth again will support R&D, Product development and Human capital creation in companies and new firms and will see profits on the mid term and long term.

An

IPO—a mechanism that once meant raising capital to fund new investment—is likely today to mark not the beginning of a new company’s greatness, but the end of it. According to a Stanford University study, innovation tails off by 40% at tech companies after they go public, often because of Wall Street pressure to keep jacking up the stock price, even if it means curbing the entrepreneurial verve that made the company hot in the first place.

Business optimism, as well as

business creation, is lower than it was 30 years ago, or that wages are flat and inequality growing. Executives who receive as much as 82% of their compensation in stock naturally make shorter-term business decisions that might undermine growth in their companies even as they raise the value of their own options.

It’s no accident that corporate stock buybacks, corporate pay and the wealth gap have risen concurrently over the past four decades. There are any number of studies that illustrate this type of intersection between financialization and inequality. One of the most striking was by economists

James Galbraith and

Travis Hale, who showed how during the late 1990s, changing income inequality tracked the go-go Nasdaq stock index to a remarkable degree.

James Kenneth Galbraith (born January 29, 1952) is an American economist who writes frequently for the popular press on economic topics. He is currently a professor at the Lyndon B. Johnson School of Public Affairs and at the Department of Government, University of Texas at Austin. He is also a Senior Scholar with the Levy Economics Institute of Bard College and part of the executive committee of the World Economics Association, created in 2011.

James Kenneth Galbraith (born January 29, 1952) is an American economist who writes frequently for the popular press on economic topics. He is currently a professor at the Lyndon B. Johnson School of Public Affairs and at the Department of Government, University of Texas at Austin. He is also a Senior Scholar with the Levy Economics Institute of Bard College and part of the executive committee of the World Economics Association, created in 2011. Travis Hale, Master of Public Affairs Program, Lyndon B. Johnson School of Public Affairs, University of Texas at Austin. Bachelor of Science, History, Science, and Technology, Georgia Tech and Bachelor of Science,, Management Science, Georgia Tech. His research interests include economic inequality, U.S. politics, and sports economics.

Travis Hale, Master of Public Affairs Program, Lyndon B. Johnson School of Public Affairs, University of Texas at Austin. Bachelor of Science, History, Science, and Technology, Georgia Tech and Bachelor of Science,, Management Science, Georgia Tech. His research interests include economic inequality, U.S. politics, and sports economics.Recently, this pattern has become evident at a number of well-known U.S. companies. Take

Apple, one of the most successful over the past 50 years.

Apple has around $200 billion sitting in the bank, yet it has borrowed billions of dollars cheaply over the past several years, thanks to superlow interest rates (themselves a response to the financial crisis) to pay back investors in order to bolster its share price. Why borrow? In part because it’s cheaper than repatriating cash and paying U.S. taxes. All the financial engineering helped boost the California firm’s share price for a while.

It is perhaps the ultimate irony that large, rich companies like

Apple are most involved with financial markets at times when they don’t need any financing. Top-tier U.S. businesses have never enjoyed greater financial resources. They have a record

$2 trillion in cash on their balance sheets—enough money combined to make

them the 10th largest economy in the world. Yet in the bizarre order that finance has created, they are also taking on record amounts of debt to buy back their own stock, creating what may be the next debt bubble to burst.

Apple has a record $2 trillion in cash on their balance sheets

Apple has a record $2 trillion in cash on their balance sheetsYou and I, whether we recognize it or not, are also part of a dysfunctional ecosystem that fuels short-term thinking in business. The people who manage our retirement money—fund managers working for asset-management firms—are typically compensated for delivering returns over a year or less. That means they use their financial clout (which is really our financial clout in aggregate) to push companies to produce quick-hit results rather than execute long-term strategies. Sometimes pension funds even invest with the activists who are buying up the companies we might work for—and those same activists look for quick cost cuts and potentially demand layoffs.

It’s a depressing state of affairs, no doubt. Yet

America faces an opportunity right now: a rare second chance to do the work of refocusing and right-sizing the financial sector that should have been done in the years immediately following the 2008 crisis. And there are bright spots on the horizon.

Despite the lobbying power of the financial industry and the vested interests both in

Washington and on

Wall Street, there’s a growing push

to put the financial system back in its rightful place, as

a servant of business rather than its master. Surveys show that the majority of Americans would like to see the tax system reformed and the government take more direct action on job creation and poverty reduction, and address inequality in a meaningful way. Each candidate is crafting a message around this, which will keep the issue front and center through November.

The American public understands just how deeply and profoundly the economic order isn’t working for the majority of people. The key to reforming the U.S. system is comprehending why it isn’t working.

Remooring

finance in

the real economy isn’t as simple as splitting up the biggest banks (although that would be a good start).

It’s about dismantling the hold of financial-oriented thinking in every corner of corporate America. It’s about reforming business education, which is still permeated with academics who resist challenges to the gospel of

efficient markets in the same way that medieval clergy dismissed scientific evidence that might challenge the existence of God. It’s about changing a tax system that treats one-year investment gains the same as longer-term ones, and induces

financial institutions to push

overconsumption and

speculation rather than healthy lending to small businesses and job creators. It’s about rethinking retirement, crafting smarter housing policy and restraining a money culture filled with lobbyists who violate America’s essential economic principles.

It’s also about starting a bigger conversation about all this, with a broader group of stakeholders.

The structure of American capital markets and whether or not they are serving business is a topic that has traditionally been the sole domain of “

experts”—the financiers and policymakers who often have a self-interested perspective to push, and who do so in complicated language that keeps outsiders out of the debate. When it comes to finance, as with so many issues in a democratic society, complexity breeds exclusion.

Finding solutions won’t be easy.

Finding solutions won’t be easy. There are no silver bullets, and

nobody really knows the perfect model for a high-functioning,

advanced market system in the 21st century. But capitalism’s legacy is too long, and the well-being of too many people is at stake, to do nothing in the face of our broken status quo. Neatly packaged technocratic tweaks cannot fix it.

What is required now is lifesaving intervention.

Crises of faith like

the one American capitalism is currently suffering can be a good thing if they lead to re-examination and reaffirmation of first principles. The right question here is in fact the simplest one: Are financial institutions doing things that provide a clear, measurable benefit to the real economy? Sadly, the answer at the moment is mostly no. But we can change things. Our system of market capitalism wasn’t handed down, in perfect form, on stone tablets. We wrote the rules. We broke them. And we can fix them.

P.S.- I have worked on and altered Rana Foroohar text in Time magazine to fit my goal to get to the core. Her text is very accurate, in-depth, professional and to the point of the financial and economical situation of the US economy. I put some encyclopedia Britannica and Wikipedia elements to the text. This was a high level financial-economical essay, with an Economist and Financial Times quality and quintessence. Good that you posted it Jaga. This is really good content, really substantive material for a Forum discussion about American Capitalism, Financialization and thus the American economy. I had to read and re-read it some times and I learned something from it. I knew the basics, but not the several layers of Financialization and the monetary policies of various American administrations (Carter, Reagan and Clinton with his New Democrat Third Way direction and policies/measures: en.wikipedia.org/wiki/New_Democrats )

I think that the only people who can reform, save and thus change the the American version of capitalism are the American voters who are the cornerstone and fundament of the American democracy. They have to vote for the best candidate, and if both parties in the Bi-partisan system would not have the right, sensible, reliable, trustworthy, intelligent, professional, experienced and rational candidate, the American voters should vote for a Third Party candidate, an Independent President. For instance Michael Bloomberg, Gary Johnson or Jill Stein. Next to the American democracy, and the American economy which is formed by American entrepreneurs, business people, workers, middle class, investors, bankers, employers and employee's, the American financial and social security is guided and served by good Commercial law or Business Law (legislation), Research and Development (innovation and new products are important to the American Capitalist economy), Human Capital (the pupils of the primary schools and highschools, and the students of the vocational universities and universities who will form the futre workforce) and scientists, economists and financial-economical journalists/experts like Rana Foroohar. The financial system should serve the real economy again. Finance should serve the needs of business by providing capital and investing in long-term growth again!